Along with expectations of an ongoing major, multi-site transaction in the ASC market in 2022, the ASC industry continued to consolidate throughout 2021. The ASC subindustry has seen recurring trends that started pre-pandemic: the shift of higher acuity procedures from the inpatient setting to the outpatient setting, increased Medicare reimbursement rates, consolidation of ASCs by management companies, and a push by hospitals to grow their ambulatory footprint with a particular focus on the outpatient setting.

COVID-19 Pandemic Recovery

For a detailed, macroeconomic analysis on the impact/recovery of the COVID-19 pandemic on healthcare M&A, please see VMG Health’s Healthcare M&A Report.

In March of 2020, the world was impacted by the spread of the COVID-19 pandemic, subsequently, 2021 was a hopeful year of rebuilding and recovering from the lasting effects brought on by the pandemic. ASC’s experienced a relatively quick recovery in 2020 with the hope that 2021 would reflect a full year of operations that mirrored pre-pandemic performance. Throughout 2021, additional variants of the original virus emerged presenting challenges for ASC’s. However, it appeared that ASCs learned from 2020 and were able to navigate the variants and continued to operate at a normal pace.

ASCs in 2021 largely had an increase in case volumes across almost all specialties, primarily due to patients willing to resume elective procedures that were postponed as well as centers keeping the doors open. Centers that were largely focused on Gastroenterology, Ophthalmology, and Otolaryngology volume were significantly hit in 2020, but have subsequently made a substantial comeback in 2021.

Shift to Higher Acuity Cases

In recent years certain higher acuity procedures that were traditionally performed in an inpatient or HOPD setting have begun to shift to a freestanding ASC setting, establishing a new standard for the level of acuity that an ASC setting could handle. The shift to more acute, higher reimbursing procedures sets up the ASC subindustry for adequate growth in the coming years, providing patients with a more cost effective and efficient manner to receive care assuming CMS regulations do not further restrict the potential cases that can be performed in the ASC setting. As discussed more in depth below, the new 2022 CMS Final Rule provides cause for concern as to whether these cases will remain in the ASC setting.

In 2021, specialties expected to increase their footprint in ASCs include Total Joint Replacements, Cardiology, and higher acuity Spine procedures. According to the most recent Ambulatory Surgery Center report published by Research and Markets, “Cardiology procedures in outpatient setting are estimated to grow from 10% in 2021 to 30-35% by mid-2020’s”. According to the same report, expectations surrounding Total Joint Replacements volume at ASC’s are expected to grow 95% over the next five years.

The higher acuity specialties have historically been a heavy lifter for revenue growth in the Hospital setting; the shift to the ASC setting will undoubtedly result in a business model shift for the Not-for-Profit and For-Profit entities managing the Hospitals. Per Tenet, parent company of USPI, the largest outpatient surgery center operator in the United States, has seen Orthopedic cases grow 22% year-over-year in 2021 and Total Joint Replacements more than double in respects to total cases. The growth opportunities provided by the outpatient care setting will likely continue to increase in the coming years and further drive the growth and consolidation of the subindustry.

Transaction Activity

In 2021, we saw a prominent large-level ASC platform player continue to expand as well as a significant number of transactions at the individual-facility level. Consistent with the observed larger platform-level transaction, the fragmented ASC industry has continued to consolidate. It is worth noting that although the industry continues along the trend of consolidation, as of 2020 approximately 72% of ASC facilities remain independent, leaving room for further consolidation at the individual-facility level. M&A activity began to pick up rapidly in 2021, furthering the shift to a more consolidated sector.

In 2020, Tenet Health finalized a deal for $1.1 billion to acquire 45 ASC’s from SurgCenter Development. Tenet further continued its efforts to consolidate in the ASC subindustry in 2021, completing a 9 ASC deal with Compass Surgical Partners. The centers included in the USPI-Compass transaction are located in Florida, North Carolina, and Texas, with 60% of the case mix coming from musculoskeletal procedures and the remaining 40% being largely ENT and ophthalmology. Additionally, in Q4 of 2021, USPI entered into a $1.2 billion deal to acquire SurgCenter Development’s remaining centers and established a long-term development deal. The transaction included acquiring ownership interest in an additional 92 ambulatory surgery centers, other support services in 21 states, and providing continuity for future de novo development projects.

“We are looking forward to adding another portfolio of high-quality, well-established SCD centers, as well as those in various stages of development. This transaction came together because of our shared commitment to quality, safety, and delivering an industry-leading experience for our patients and physicians alike. We are excited to continue our longstanding relationship in partnership with the SCD principals, who have an extremely effective development engine to expand our network of care.” – Ron Rittenmeyer, Executive Chairman & CEO

Ascension Capital, an investment arm of Ascension and Towerbrook Capital Partners, invested in Regent Surgical Health in 2021 to act as the development partner to spearhead future growth opportunities. Additionally, HCA Healthcare announced in Q1 2021 that it intends on investing in 10 to 12 new ASCs. Per HCA CEO, Sam Hazen, “We continue to invest broadly across our networks to improve convenience, access, and value for patients by developing more outpatient facilities. The pipeline for development and acquisition in this category remains strong.” Lastly, in May 2021 Surgery Partners, inc. and UCI Health announced, “A new strategic partnership that marks an expansion of community access to outpatient surgical facilities for nearly 4 million residents throughout Orange County, western Riverside County and southern California,” per Surgery Partners news release. As of December 31, 2021, the largest operators (in terms of number of ASCs) are United Surgical Partners International (USPI), Envision Healthcare/Amsurg Corporation, and Surgical Care Affiliates (SCA), with ownership of approximately 430+, 250+, and 250+ ASCs, respectively. As noted in the chart below, the number of total centers under partnership by a national operator, as a percentage of total Medicare certified centers, saw an increase from 2021 to 2022 growing from approximately 1,725 centers to 1,752 centers. Additionally the top 5 management companies have increased the number of centers under management by approximately 441 centers since 2011, which represents a compound annual growth rate of 4.76%. As management companies have increased in size, they are able to increasingly provide a greater level of strategic value by bringing greater leverage with commercial payors, enhanced management and reporting capabilities, and improved vendor contracts to acquisition targets.

Reimbursement

On November 1, 2020, the Medicare reimbursement fee schedule for ASCs in 2021 was finalized by the Centers for Medicare & Medicaid Services (CMS). Consistent with previous years, For CYs 2019 through 2023, CMS will update the ASC payment system using the hospital market basket update, rather than the Consumer Price Index for All Urban Consumers (CPI-U). CMS published the 2021 ASC payment final rule, which resulted in overall expected growth in payments equal to 2.4% in CY 2021. This increase is determined based on a hospital market basket percentage increase of 2.4% less the multifactor productivity (MFP) reduction of 0.0% mandated by the ACA. Moreover, the ASC payment final rule for CY 2022 was released by CMS on November 2, 2021, resulting in overall expected growth in payments equal to 2.0% in CY 2022. This increase is determined based on a projected inflation rate of 2.7% less the MFP reduction of 0.7% mandated by the ACA. The ASC subindustry sees the 2021 and 2022 reimbursement increases as a win as CMS continued to follow its proposal to align update factors, moving ASCs to the hospital market basket which historically was used to update HOPD payments. Under the final rule, CMS will use the hospital market basket to update ASC payments through CY 2023.

The table below reflects a summary of the estimated Medicare ASC payments for 2020, 2021 and 2022 for the top 10 CPT codes performed in ASCs in 2021. As noted below, the observed 2021 payments by Medicare for the top 10 CPT codes for 2021 is projected to increase 1.2% through the estimated 2022 payments.

Procedures

In the 2021 CMS Final rule, 267 surgical procedures were added to the ASC payable list. On July 19, 2021, CMS proposed the 2022 Hospital Outpatient Prospective Payment System and ASC Payment System, which proposed the removal or reversal of 258 procedures from the ASC payable list back to the Inpatient-Only (IPO) list. In the newly released final rule on November 2, 2021, CMS revised the previous CPT Code removal list and ultimately removed 255 procedures, removing from the list CPT Codes 22630 (Lumbar spine fusion), 23472 (Reconstruct ankle joint) and their corresponding anesthesia codes. Furthermore, in 2022 CMS is working on the reinstatement of the inpatient-only list and returning the CPT Codes that were removed from the list in 2021.

Overall, the 255 surgical procedures being placed back on the IPO list in 2022 are generally higher acuity, higher reimbursing cases. Not only could the loss of these higher reimbursing procedures result in a loss for respective ASC’s, but the center’s that devoted time and capital to acquire the necessary equipment to perform these procedures would be out a significant amount in terms of useful capital expenditures.

In addition, CMS is finalizing proposals to the Ambulatory Surgical Center Quality Reporting (ASCQR) programs to help facilitate measurement and reporting for quality of care in the outpatient setting. The ASCQR is “a pay-for-reporting”, quality data program administered by CMS. Under this program, ASCs report quality of care data for standardized measures to not receive a payment penalty to their annual payment update to their ASC annual payment rate. CMS has listed a variety of measurements and qualifications that the ASC’s must adhere to, as mentioned above, violation of the procedures will result in a reduction in 2.0% in their annual fee schedule update. The 2.0% adjustment follows the 2019 final rule that applied the market hospital market basket update to ASC payment rates.

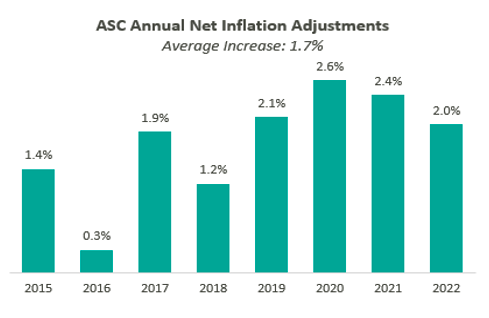

Presented in the chart below is a summary of the historical net inflation adjustments for CY 2015 through CY 2022. The annual inflation adjustments are presented net of additional adjustments, such as the MFP reduction, outlined in the final rule for the respective CY. The CY 2022 inflation adjustment continues the trend of relative stability of annual adjustments since CMS implemented the use of the hospital market basket update to finalize payment rates in CY 2019.

Overall, the final ruling to increase ASC payments by CMS and increased recovery from COVID-19 would both indicate an expected increase in total ASC payments. This increase is partially offset by the removal of the 255 generally higher reimbursing CPT codes that were removed with the CY 2022 final rule. Ultimately, CMS has projected total ASC payments in 2022 to increase approximately $40 million from 2021 payments, to be approximately $5.41 billion.

In conclusion, we began to see a return to pre-Covid normalcy in 2021. Case volume returned to historical levels as patients began to become more confident in their ability to receive medical attention and have elective procedures in a healthy and cost-effective manner. Although the removal of certain higher acuity procedures detailed in the CMS final rule will result in a negative impact to ASC’s, expectations for 2022 are a continued increase in growth and consolidation in this subindustry. The ASC setting provides a convenient, cost-effective way for patients to receive high-quality care. Overall, ASCs at the center level are expected to continue the positive momentum started in 2021 and the subindustry as a whole is expected to see a large number of transactions in 2022.

At the Becker's 23rd Annual Spine, Orthopedic and Pain Management-Driven ASC + The Future of Spine Conference, taking place June 11-13 in Chicago, spine surgeons, orthopedic leaders and ASC executives will come together to explore minimally invasive techniques, ASC growth strategies and innovations shaping the future of outpatient spine care. Apply for complimentary registration now.